.png?width=357&height=85&name=tpiq-logo%20(375x85).png "TaxPlanIQ")

- 4 min read

- Share via:

- Copy link

We’ve covered the “3 P’s of Tax Planning” a couple of times on the TaxPlanIQ blog. In part one, it was the overview of the system. Part two covered how people play an integral role in your firm’s success.

This article (the finale, aka “part three”) is a bit of an in-depth look at the two other “P’s” — Pricing and Product.

You’ll see:

- How to sever the link between time and firm revenue (i.e. hourly billing)

- What the product becomes, when it’s no longer you

- How to communicate this change in a way that excites your clients

Pricing

“There are only so many hours you can work.” — Ron Baker

Pricing time, either yours and/or your team's, is a burden to growth. It’s a constraint. Not a value to you or your clients.

Think about it in a couple of ways. One, when you’re growing quickly (in terms of the number of clients you serve) the only way to grow is by adding hours.

You pay $50k+ per year to another accountant hire (which isn’t easy to do with a staffing shortage), and they generate 2-3x their salary in revenue, if they’re efficient.

Tying hours to dollars means the better you get the less you make.

You're not exactly scaling there, and you’ll soon wind up with more clients to deal with than a single owner should.

The other way of improving revenue in hourly pricing is to do more in less time, freeing up the time to serve more clients (with the same amount of staff). This solution is, of course, not infinitely scalable.

And if you think about it, the better you are and fulfilling services (i.e. faster), the less you’re getting paid.

Enter Value Pricing

Not going to spend a ton of words here. But if you’re interested, we outline value pricing in this post.

In short, value pricing is charging for the benefit of your expertise, specific strategies, and return on investment for what you do.

In order to value price, you have to offer something of value. Good news, you already do that every day. The piece that’s missing is you have to communicate that value properly, showing clients the value of what they’re getting from your firm.

A Word on Ethical vs Contingent Fees

“Isn’t value pricing unethical?”

This is a common question from firm owners. And there is a necessary distinction between value pricing and something called “contingent fees.”

Contingent fees are based on results, and paid after the results are seen. So, someone says, “If I save you $XX thousands by restructuring your entity, you pay me XX% of those savings.”

This is unethical.

Value pricing fees are collected up front. And in the case of tax planning, they are based off of the agreed upon tax strategy you’ve presented to a client.

So, you’ve had a discovery call with a client, researched the best tax strategies for their particular nexus. Then, you have a meeting to discuss the following:

- Each particular strategy you would offer them (for this coming year and amendments, if any).

- The amount of potential tax savings, based on their current financial situation.

- Other services and benefits included with your services.

- The initial cost to implement these strategies and the ongoing cost.

Then, ideally they say “yes,” pay the initial amount, and your team gets to work.

Key point: Value is pre-payment for strategy, advice, and work — not for guaranteeing results.

Product

Before we begin, say (or think) the following statement: “I am not the product.”

When you move away from hourly pricing, it’s important to sever the connection between your actual work and revenue—shifting it to…what, exactly?

If you’re not the product (aka number of hours to do the work), what is the widget you offer to clients in exchange for your pricing?

Answer— It’s the tailored tax strategy, implementation of said strategy, other included features/benefits.

Let’s quickly cover each:

Tailored Tax Strategy

Accounting firms are busy. This time constraint often results in clients overpaying on taxes. There are hundreds of tax-saving credits, deductions, and individual strategies. Your clients don’t know any of them, and frankly, most accountants don’t either.

Showing clients they’ve overpaid is a shock. It gets their attention. And showing them the strategies to rightfully keep their money convinces them you’re qualified to handle their tax plan.

Strategy Implementation

Accountants know about a lot of strategies, but there are nuances, hurdles, and red tape to many of them. These take time (i.e. hours) which you don’t have, if you’re hourly-based. But if the strategy gives a great ROI for your client, they’ll pay you a fair amount to overcome all of the challenges in a given strategy.

And you’ll want to do the work!

Tip: TaxPlanIQ offers steps, tasks, and helpful resources for dozens of common tax strategies to help save your clients’ money.

Peripheral Features and Benefits

Trading time for money means every interaction you have with a client costs them money and you time. It’s naturally contentious and leads to both parties avoiding the other.

But value pricing is set, either in phases or monthly.

This means you’re able to do the work as fast as possible, benefiting from things like automation and workflow management. That said, you’ll also want to offer the client another value—the option to get help when they need it.

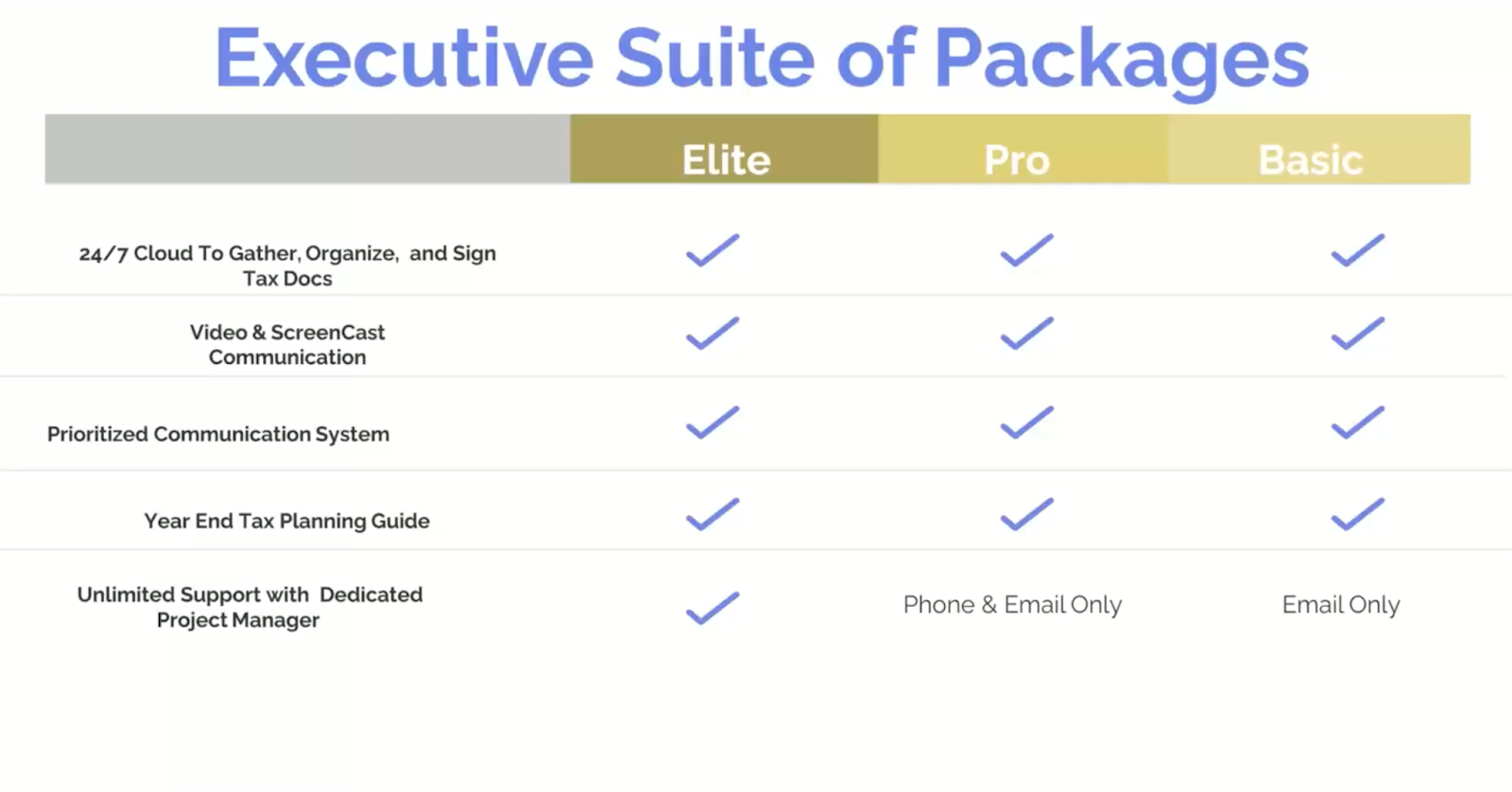

Here’s an example of benefits a firm may offer:

Things like priority communication, multiple methods for them to get help, and even content that allows them to help themselves are great value-adds to your tax planning.

Pricing, Product, and People — The Keys to Scale Your Firm

Put your people first by communicating the value of your products, and price them in a way that allows you to successfully run your business.

Clients want to know their tax planner understands their unique situation and how to get their tax burden down to where it should be. You convince them of that by highlighting the product (strategy, implementation, and service).

And that makes your price worth it to the right customers.